Smart Personal Finance for Indian Investors.

From mutual funds and home loans to credit cards and tax planning - Invest With Bull breaks down complex money topics into clear, actionable advice. Whether you are building wealth, planning your first home, or optimizing your credit card rewards, you are in the right place.

EPFO Interest Rate 2026 Update: 8.25% Retained! What It Means for Your PF & Mutual Fund Strategy

March 1, 2026 | by Amit Sharma

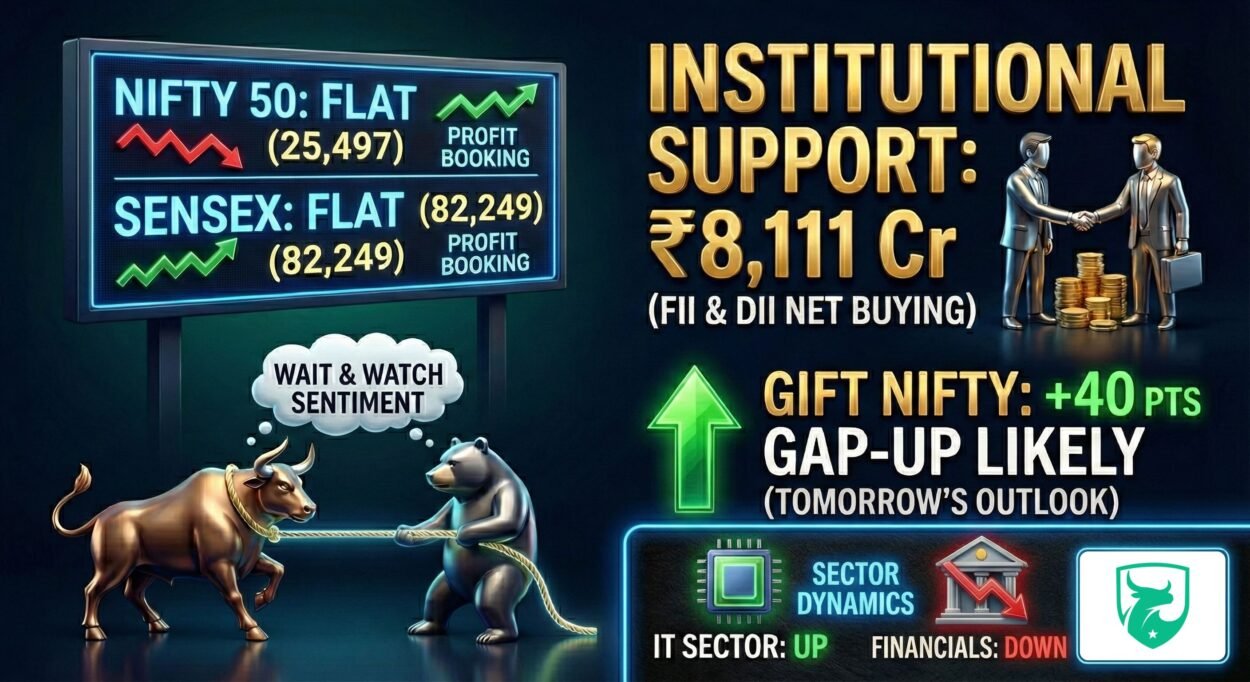

Market Daily: Dalal Street Consolidates as ₹8,111 Cr Institutional Inflow Cushions Dips

February 26, 2026 | by Amit Sharma

Triveni Engineering (TRIVENI): A Deep Dive into the ₹1.50 Dividend and Q3 Surge

February 25, 2026 | by Amit Sharma

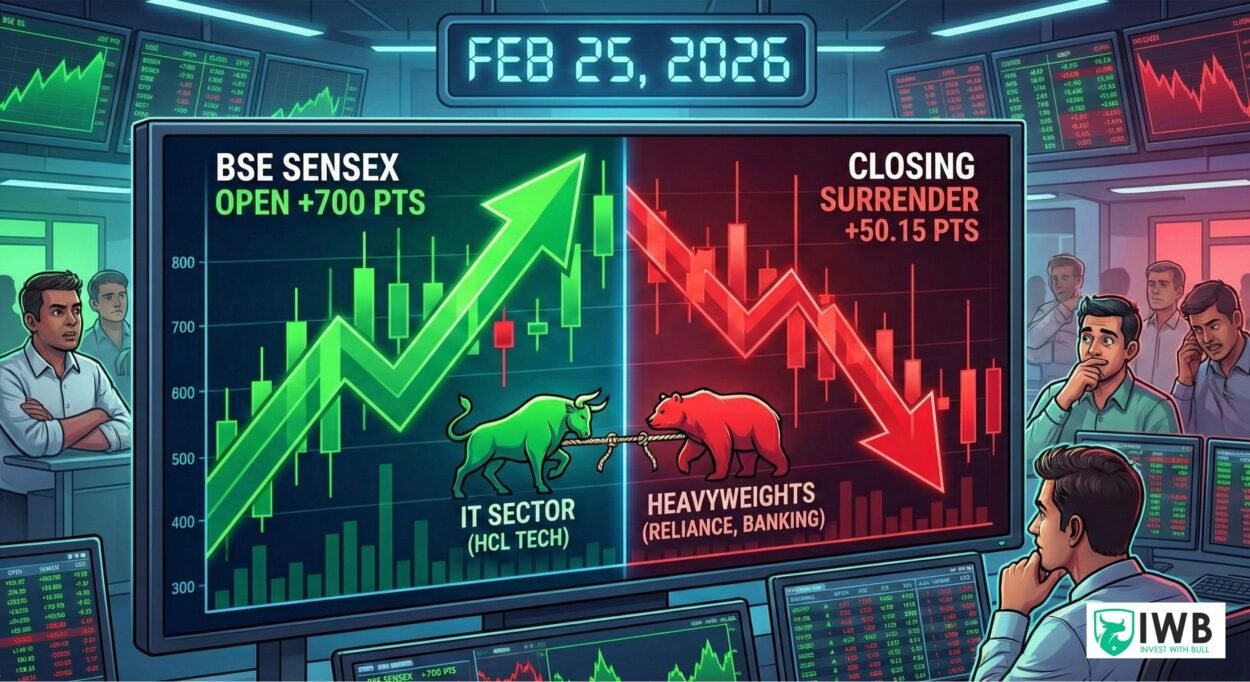

Market Wrap: The Intraday Trap – Sensex Surrenders Early Gains as Heavyweights Drag

February 25, 2026 | by Amit Sharma

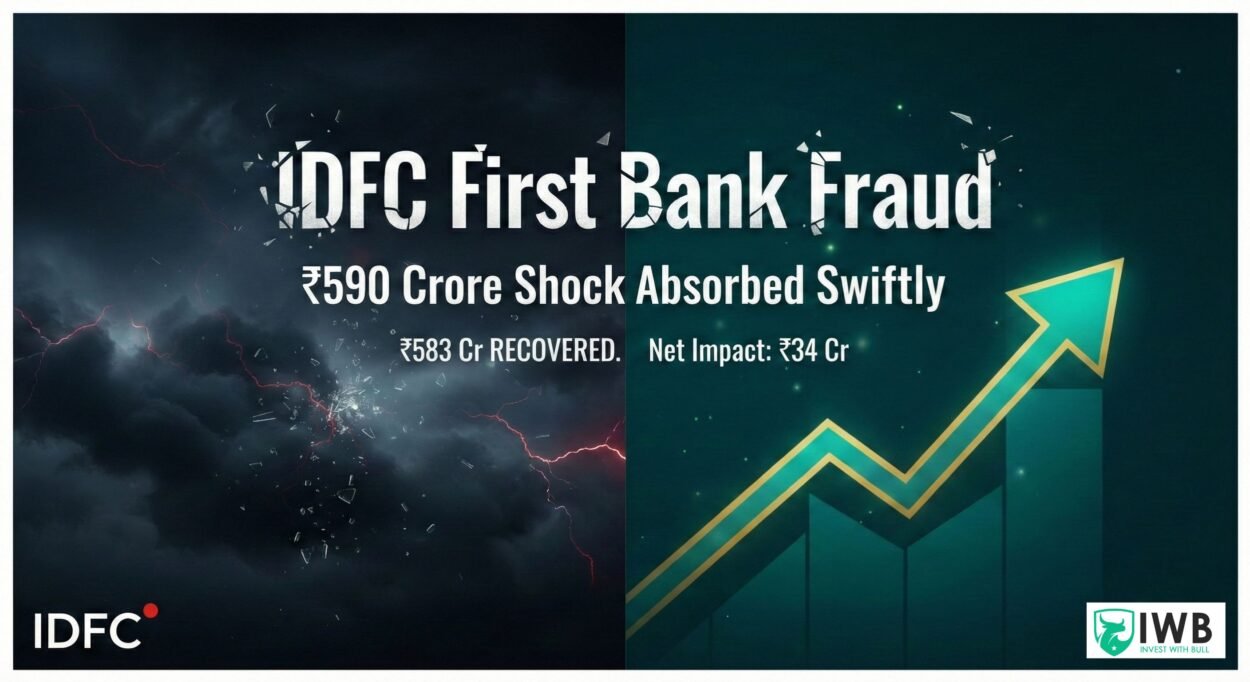

IDFC First Bank Recovers ₹556 Crore Following Branch Fraud; Stock Stabilizes After 20% Dip

February 25, 2026 | by Amit Sharma

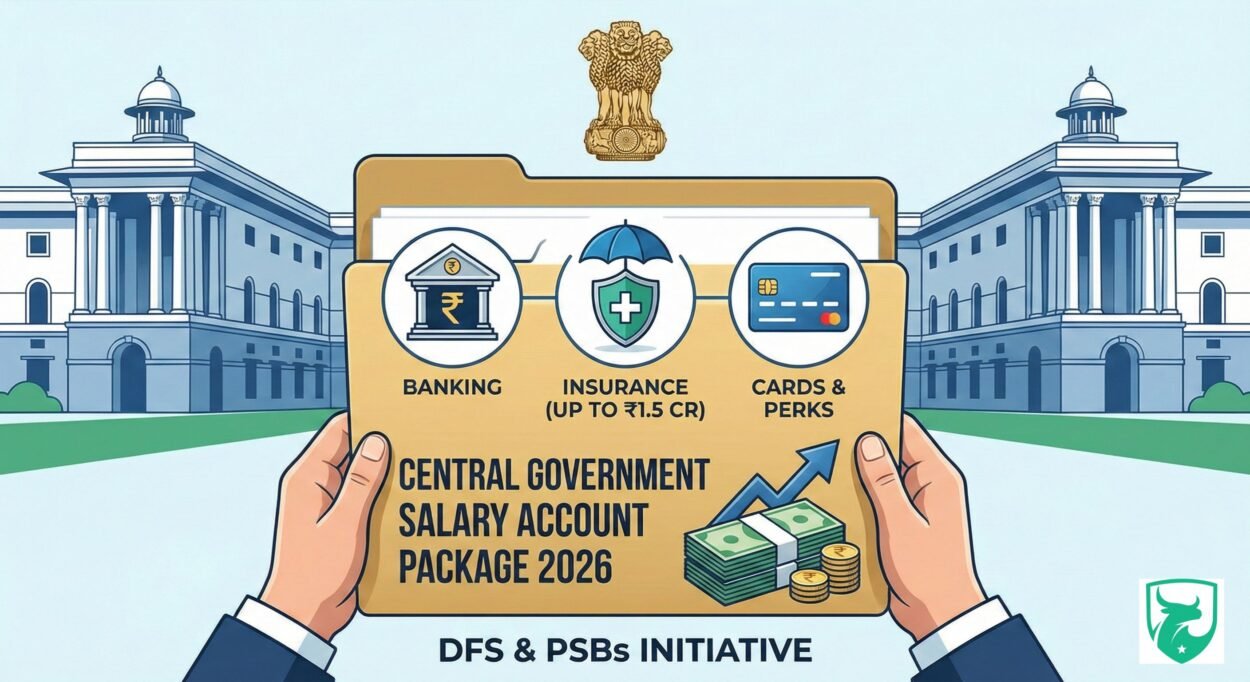

The Hidden Wealth in the New Central Government Salary Package

February 25, 2026 | by Amit Sharma

The India-France Tax Treaty Overhaul: Navigating the New 15% Dividend Hit

February 25, 2026 | by Amit Sharma

How Much More Money Will You Take Home After Budget 2026? New Income Tax Rules Explained for Salaried Indians

February 23, 2026 | by Amit Sharma

Fuel Your Savings: The Complete 2026 Guide to the BPCL SBI Credit Card

February 23, 2026 | by Amit Sharma

Best investments in India 2026: Where to Invest in India in 2026 for Long-Term Wealth

February 22, 2026 | by Amit Sharma

The 2026 Union Budget “Tax Trap”: Why Your Salary Hike is a Hidden Pay Cut

February 22, 2026 | by Amit Sharma

Curious about the EPFO interest rate 2026? If you are a salaried professional in India, your Employee Provident Fund (EPF) is likely one of the most critical pillars of your retirement planning. This specific rate has been the biggest trending topic in Indian finance circles recently, and the verdict is finally in.

Welcome to the ultimate guide by Invest with Bull. Today, we are compiling everything you need to know about the latest March 2026 EPFO announcements, the historical context, the exact math behind your returns, and how you should position your portfolio using a mix of EPF and high-growth mutual funds (mut).

The Big News: 8.25% Retained for FY 2025-26

Leading up to the March 2026 Central Board of Trustees (CBT) meeting, there was intense speculation about a potential rate cut to the 8.00% bracket. However, the EPFO has decided to retain the interest rate at a solid 8.25% for the third consecutive year!

With global rate volatility and millions of new subscribers joining under government employment schemes, retaining this rate is a massive win for the working class. It ensures capital protection while providing a steady yield that beats traditional fixed deposits. For official circulars, you can always monitor the official EPFO portal.

The Game Changer: EPFO Wage Ceiling Increase

While everyone is focused on the interest rate, a massive structural update is underway: the potential hike in the EPFO wage ceiling.

Currently, mandatory EPF contributions are capped at a basic salary of ₹15,000 per month (a limit set in 2014). Following Supreme Court directives, the EPFO is actively looking to raise this ceiling to ₹25,000 per month.

If implemented, millions of mid-skilled workers will be brought into the mandatory social security net. Your monthly take-home pay might decrease slightly, but your mandatory retirement corpus will compound at an unprecedented rate.

EPFO Interest Rate History: The Last 10 Years

To gauge the long-term reliability of this retirement fund, investors constantly look up the EPFO interest rate history. The EPF has never dropped below 8% since 1977-1978.

Here is the official EPF interest rate last 10 years trend so you can visualize your compounding wealth:

| Financial Year | Declared Interest Rate | Status |

| 2025 – 2026 | 8.25% | Retained |

| 2024 – 2025 | 8.25% | Credited |

| 2023 – 2024 | 8.25% | Credited |

| 2022 – 2023 | 8.15% | Credited |

| 2021 – 2022 | 8.10% | Credited |

| 2020 – 2021 | 8.50% | Credited |

| 2019 – 2020 | 8.50% | Credited |

| 2018 – 2019 | 8.65% | Credited |

| 2017 – 2018 | 8.55% | Credited |

| 2016 – 2017 | 8.65% | Credited |

The Exact PF Interest Rate Calculation Formula

A common misconception is that your annual interest is simply multiplied by your year-end balance. In reality, the EPFO calculates your interest on a monthly running balance, even though it is credited annually.

Here is the official PF interest rate calculation formula:

How it works in practice:

If your opening balance for the month is ₹1,00,000 and the current annual rate is 8.25%:

- Divide the annual rate by 12: $8.25 \div 12 = 0.6875\%$ per month.

- Apply it to the balance: $1,00,000 \times 0.6875\% = \text{₹}687.50$.

- This ₹687.50 is recorded for that month. The system repeats this, sums up the 12 months, and deposits it at the end of the financial year.

Looking Ahead: EPFO Interest Rate 2026 27 Projections

What happens next year? Economists are already mapping out the EPFO interest rate 2026 27 projections.

If the proposed wage ceiling hike (₹15,000 to ₹25,000) is fully implemented, the EPFO will manage an unprecedented influx of funds. To maintain the stability of this expanded corpus, financial experts predict the CBT may adopt a highly conservative approach next year, potentially stabilizing the rate permanently in the 8.00% to 8.15% corridor to protect capital buffers.

The “Invest with Bull” Verdict: EPF vs. Mutual Funds

Relying solely on your EPF for retirement is a strategy of the past. While an 8.25% tax-free return is a fantastic debt instrument, it will barely beat long-term lifestyle inflation.

To build aggressive, generational wealth, your EPF needs a companion.

- Treat EPF as your Debt Safety Net: It provides sovereign-backed capital protection.

- Fuel your Growth with Mut (Mutual Funds): Channel your surplus income into high-growth equity mutual funds. A disciplined SIP in a Nifty 50 index fund or a Flexi-cap fund historically delivers 12% to 15% long-term returns.

By balancing the guaranteed returns of the EPFO with the aggressive growth of the stock market, you create a bulletproof financial fortress. Check out our ultimate guide to building a winning mutual fund portfolio to get started today.

Frequently Asked Questions (FAQs)

What is the current EPFO interest rate for 2025-2026?

The Central Board of Trustees has opted to retain the interest rate at 8.25% for FY 2025-26, marking the third consecutive year at this rate.

When is the EPF interest credited to my account?

Interest is calculated on your monthly closing balance but is credited to your EPF account annually at the end of the financial year (typically starting around March or April).

How can I check my EPF balance online?

You can check it via the UMANG App, the official EPFO Member e-Sewa portal, by sending an SMS (EPFOHO UAN ENG to 7738299899), or by giving a missed call to 9966044425 from your registered number.

Is the interest earned on EPF taxable?

EPF interest is completely tax-free up to an annual contribution limit of ₹2.5 lakh for private-sector employees. Interest earned on contributions exceeding this limit is taxed according to your income tax slab.

Will the proposed wage ceiling hike affect my take-home salary?

If the ceiling increases to ₹25,000, your mandatory 12% contribution will be calculated on a higher base. Your take-home pay might slightly decrease, but your long-term retirement savings will grow much faster.