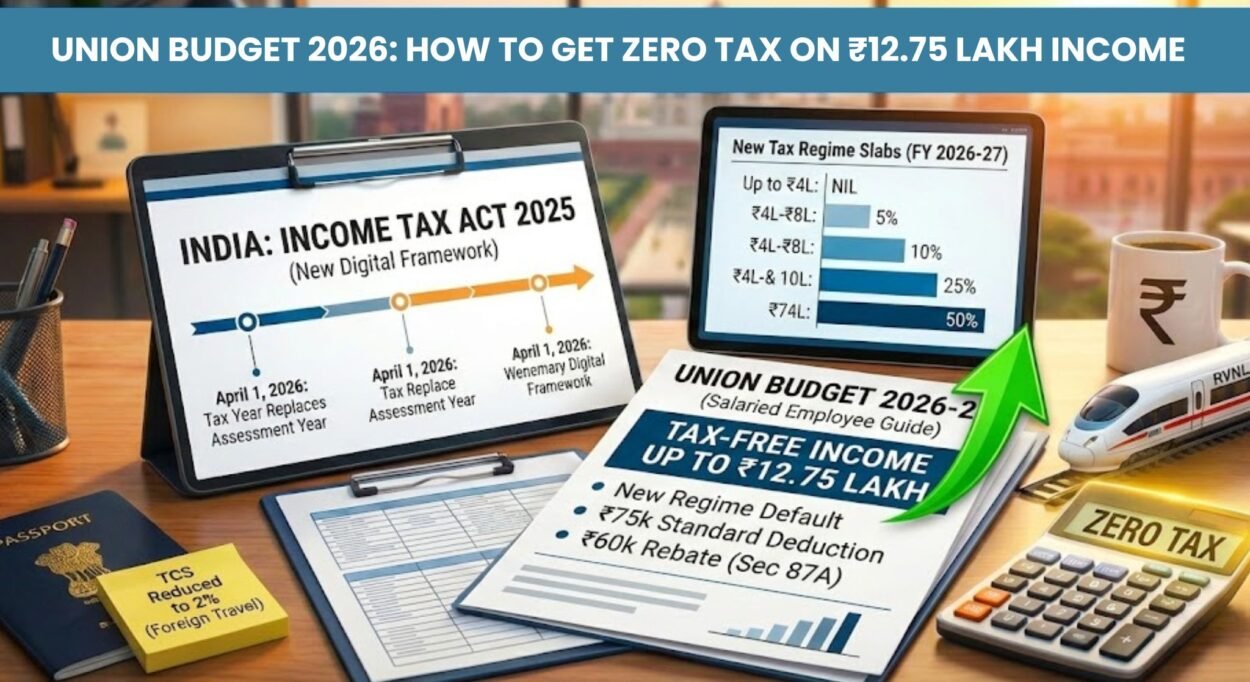

How Much More Money Will You Take Home After Budget 2026? New Income Tax Rules Explained for Salaried Indians

Published: 23/02/2026 | by Amit Sharma

How Much More Money Will You Take Home After Budget 2026? New Tax Rules Explained for Salaried Indians

| Aspect | Old Regime (typical till 2025) | New Tax Rules 2026 (new regime direction) |

|---|---|---|

| Core idea | Many exemptions/deductions, higher tax rates | Fewer deductions, simpler slabs, relatively lower rates |

| Best suited for | Heavy tax planners (home loan, ELSS, NPS, etc.) | Simple salary earners with moderate investments |

| Complexity | High – lots of proofs and paperwork | Lower – straightforward slabs and calculations |

| Budget 2026 tilt | Mostly status quo, limited tweaks | Clear push to make it the default and more rewarding |

How Much More Will You Take Home? Illustrative Salary Examples

Now to the most practical part: what happens to your in‑hand salary. Below are conceptual examples for three salary levels. These are to show direction; your actual numbers will depend on the final slabs, your CTC structure, and your deductions.

Sample table for ₹12L income

| Scenario | Old Regime (approx annual tax) | New Regime 2026 (approx annual tax) | Approx Extra In‑Hand Per Month |

|---|---|---|---|

| Salaried, ₹12L, basic deductions only | ₹1,60,000 | ₹1,40,000 | ~₹1,700 per month higher in‑hand salary |

1. Around ₹7 lakh per year (early or junior salaried)

Assumptions (illustrative):

- Annual CTC: ₹7,00,000

- Simple salary structure with limited additional deductions

- Old regime: basic 80C investment, some standard benefits

- New regime 2026: more liberal slabs, minimal deductions

Likely trend:

- At this income, many salaried individuals may end up paying very little tax or coming close to zero effective tax under the new rules, depending on how the slabs and rebates are structured.

- This translates into a noticeable improvement in monthly in‑hand salary – possibly from a few hundred to a couple of thousand rupees more each month in many cases.

2. Around ₹12 lakh per year (typical urban middle class)

Assumptions (illustrative):

- Annual CTC: ₹12,00,000 (around ₹1 lakh gross per month)

- Old regime: uses 80C (ELSS/EPF/PPF), 80D (health insurance), some HRA

- New regime 2026: simpler slabs with lower rates but limited deductions

Likely trend:

- For this bracket, Budget 2026 tries to ensure that even if you are not doing aggressive tax planning, your effective tax rate under the new rules is slightly lower.

- At a broad level, this can mean annual tax savings in the range of several thousand to around ₹15,000–₹25,000 for many salaried people, which feels like an extra ₹1,000–₹2,000 per month in hand.

3. Around ₹20 lakh per year (upper‑middle salaried)

Assumptions (illustrative):

- Annual CTC: ₹20,00,000

- Old regime: fully uses 80C, home loan interest, NPS, etc.

- New regime 2026: somewhat softer slabs but limited tax breaks

Likely trend:

- At this level, tax outgo will still be significant, but a slightly more favourable slab structure in the new regime can offer some percentage‑point relief, especially if you prefer simplicity over heavy paperwork.

- If you were already maximising all possible deductions in the old regime, the difference may not be dramatic, but you gain in terms of simpler compliance and fewer moving parts.

What Happens to 80C, 80D and Your Tax‑Saving Investments?

One of the biggest behavioural shifts after the new tax rules is that the pressure of “investing only to save tax” is slowly reducing, especially if you opt for the new regime.

- Section 80C (ELSS, PPF, EPF, life insurance, home loan principal)

- Under the old regime, 80C remains a key pillar, and for those who still choose it, these investments will continue to matter.

- Section 80D (health insurance premiums)

- Health insurance remains essential, regardless of regime, because the primary purpose is protection, not just tax saving.

- Home loan interest / HRA

- Housing‑linked benefits are still a major factor in deciding which regime is better for a particular taxpayer.

Overall, the focus is gradually shifting from “buy products just to save tax” to “use products for real wealth creation and protection,” because the rules are pushing towards simplification.

Tax‑saving investments under Section 80C

SIPs, ELSS, Insurance and Loans: How to Think in 2026

Under the new tax rules, you should re‑look at four core areas of your financial life.

- SIPs and Equity Mutual Funds

- Continue systematic investment plans primarily for long‑term wealth creation, not only for tax breaks, especially if you adopt the new regime.

- ELSS vs Other Equity Funds

- Under the old regime, ELSS remains one of the most efficient tax‑saving options; under the new regime, a simple diversified equity fund may be more logical if tax saving is less of a driver.

- Life and Health Insurance

- Prioritise a solid term plan and health cover for risk management; Budget 2026 and most expert checklists emphasise financial security as a core foundation.

- Personal Loans and High‑Cost Debt

- Any extra in‑hand salary you get after Budget 2026 is a good opportunity to pre‑pay high‑interest personal loans and credit card dues. Many 2026 personal finance guides advise debt reduction as a key theme.

How to Start SIP in Mutual Funds

Five Practical Steps You Should Take Now

To make the most of the new tax rules 2026, here are five simple, actionable steps.

- Compare the Old and New Regimes for Your Exact Situation

- Use online calculators or speak to a CA to compare both regimes using your actual income, investments, and deductions. Do this once properly, then stick to the better one.

- Talk to HR About Optimising Your Salary Structure

- Review HRA, allowances, reimbursements, and PF contribution to align with the regime you plan to choose, so that your post‑Budget 2026 in‑hand is maximised.

- Realign Your Investments With Your Goals

- Move away from buying products only for tax benefits and instead build a portfolio that covers emergency fund, SIPs for goals, and adequate insurance.

- Adopt an Annual Personal Finance Checklist

- At least once a year, review income, expenses, loans, insurance, investments, and tax. Many 2026 checklists recommend setting one fixed “money review date” to stay disciplined.

- Strengthen Your Documentation and On‑Time Filing

- Even with simpler rules, keep proofs, track Form 16/Form 26AS, and file your ITR on time to avoid notices or penalties. Simplification does not mean you can be careless.

FAQs on Budget 2026 and the New Tax Rules for Salaried People

Do I have to compulsorily move to the new regime in 2026?

The government is clearly nudging taxpayers towards the new regime and making it the default, but in many cases you will still have an option to choose your regime, especially if you have significant deductions under the old system.

If my salary is around ₹10–₹12 lakh, which regime is likely to be better?

It depends on how much you invest and claim under sections like 80C, home loan interest, NPS and insurance. For those with simple salary and limited deductions, the new regime under the 2026 rules often works out better; heavy planners may still benefit from the old regime.

Should I stop investing in ELSS or SIPs after the new rules?

No. If your primary goal is wealth creation, continuing ELSS and SIPs can be very beneficial over the long term. You should not abandon good long‑term products only because the tax angle changes slightly.

From when will the new tax rules 2026 actually apply?

The changes apply to income earned in the financial year 2026–27 (starting 1 April 2026), with the assessment year coming after that. Always check the latest official notifications for final dates and provisions.

As the Lead Analyst at Invest With Bull, Amit Sharma bridges the gap between complex banking regulations and your wallet. With a core focus on Credit Card Arbitrage and BDA Real Estate, Amit provides the data-backed analysis that salaried professionals need to maximize returns and minimize interest. He is dedicated to building financial literacy through unbiased, actionable research.

RELATED POSTS

View all