If you feel like credit cards are a “grown-up” mystery, you aren’t alone. In 2026, the financial world moves fast, with digital wallets, UPI-linked credit lines, and AI-driven spending insights.

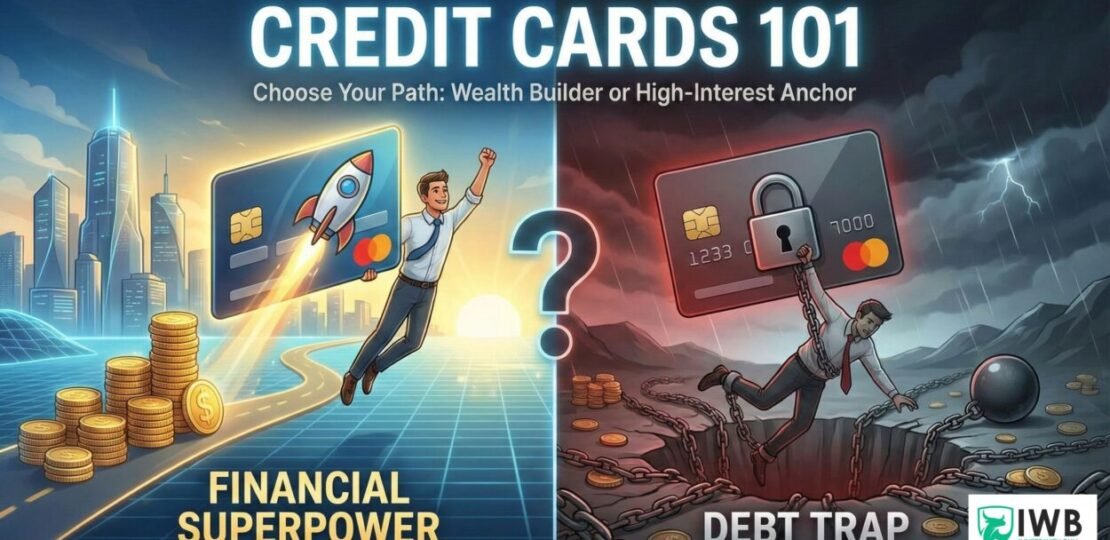

But at its core, a credit card is simple: it’s a tool. Used correctly, it’s a financial superpower that earns you free travel and builds your credit score. Used poorly, it’s a debt trap with interest rates as high as 20% or more.

This guide breaks down everything you need to know, even if you have zero finance knowledge.

1. What Exactly is a Credit Card?

Think of a credit card as a pre-approved loan in your pocket.

Debit Card: You spend your own money (from your bank account).

Credit Card: You spend the bank’s money. At the end of the month, the bank sends you a bill to pay them back.

credit vs debit infographic

2. Key Terms You Must Know (The “Jargon Buster”)

You don’t need a finance degree, just these four terms:

Credit Limit: The maximum amount the bank allows you to borrow. If your limit is $2,000, you can’t spend $2,001.

Statement Balance: The total amount you spent during the last 30 days. This is the number you want to pay off in full.

APR (Annual Percentage Rate): This is the cost of borrowing. If you don’t pay your bill in full, the bank charges you interest based on this percentage. According to the Federal Reserve, average rates are currently around 20-22%.

Minimum Payment: The smallest amount you can pay to avoid late fees. Warning: This is the “Trap.” Only paying the minimum means your debt will keep growing.

3. How to Use a Credit Card Like a Pro

To turn this tool into a superpower, follow the Golden Rules of 2026:

Use the “Grace Period” to Your Advantage

The Grace Period is the 21-25 day window between when your bill is generated and when it’s due. If you pay the Full Statement Balance by the due date, you pay $0 in interest. It is literally a free loan.

Master the 30% Rule (Credit Utilization)

Your Credit Utilization Ratio is a fancy way of saying “how much of your limit you use.”

The Math: If your limit is $1,000 and you spend $300, your utilization is 30%.

The Goal: Keep this under 30% to see your credit score skyrocket.

Visualizing financial success: A high credit score of 750 on a range of 1-900, symbolizing strong creditworthiness and financial stability.

4. Why Bother? The Superpower Perks

Why not just use a debit card? Because credit cards offer protections that cash doesn’t:

Fraud Protection: If someone steals your credit card info, the bank’s money is at risk, not yours. You are usually not liable for fraudulent charges.

Credit Building: A high credit score helps you get lower interest rates on car loans and home mortgages later in life.

Rewards & Cash Back: Many cards pay you to use them. Imagine getting 2% back on every grocery trip or enough points for a free flight to Bali.

Internal Link:Want to earn more? Read our guide on [How to Maximize Credit Card Rewards in 2026].

5. The “Debt Trap”: How People Get Into Trouble

The trap isn’t the card; it’s the mindset.

Treating it as “Extra Money”: If you have $500 in your bank account, don’t spend $600 on your card.

Cash Advances: Avoid taking cash out of an ATM with a credit card. Interest starts the second that cash hits your hand, and the fees are massive.

Which Card Should You Pick? (2026 Comparison)

Card Name

Best For

Annual Fee

Key Benefit

Amazon Pay ICICI

Amazon Loyalists

Nil (Lifetime Free)

5% Cashback for Prime members

SBI SimplyCLICK

Online Shopping

₹499 (Waived at ₹1L spend)

10X Points on Apollo, BookMyShow, Cleartrip

Axis Bank ACE

Utility Bills & GPay

₹499 (Waived at ₹2L spend)

5% Cashback on Bill Payments via GPay

1. Amazon Pay ICICI (The “Set it and Forget it” Card)

If you hate the idea of paying an annual fee, this is the gold standard. It’s Lifetime Free (LTF), meaning it costs you ₹0 to keep in your wallet.

The Perk: You get 5% back on Amazon (if you’re a Prime member) and 2% back on 100+ partner merchants like Uber and Swiggy.

The Hook: The cashback is credited directly to your Amazon Pay balance—no manual redemption needed.

2. SBI SimplyCLICK (The “Digital Native” Card)

This card is perfect for someone who does everything online—from ordering medicine on Apollo 24×7 to booking flights on Cleartrip.

The Perk: You get a ₹500 Amazon Voucher just for joining, which effectively makes the first year free.

The Hook: 10X reward points on partner brands like Myntra and Yatra.

3. Axis Bank ACE (The “High-Value” Card)

While it has a fee, the Axis ACE often pays for itself. It is one of the best cards in India for Unlimited Cashback.

The Perk: 5% cashback on utility bills (Electricity, Internet, Gas) and mobile recharges made via Google Pay.

The Hook: 1.5% unlimited cashback on all other spends, which is higher than most beginner cards.

Pro-Tip: The “RuPay” Factor

In 2026, many of these cards now come in a RuPay variant. If you have the choice, pick RuPay! It allows you to link your credit card to UPI apps (like BHIM or PhonePe) so you can scan any merchant QR code and pay using your credit limit instead of your bank balance.

Frequently Asked Questions (FAQs)

Q1: Does opening a credit card hurt my score?

When you apply, there is a “Hard Inquiry,” which might drop your score by a few points temporarily. However, in the long run, having a card and paying it on time will significantly increase your score.

Q2: Is there a “Best First Credit Card” for beginners?

In 2026, Secured Credit Cards or Student Cards are the best starting points. They have lower limits and are easier to get if you have no credit history. Check out our Top 7 Credit Cards for salaried 2026

Q3: What if I can’t pay the full balance one month?

Pay as much as you can above the minimum. This reduces the amount of interest you’ll be charged. If you’re struggling, call your bank—many have “hardship programs” to help you avoid a “Charge-Off” (which ruins your credit for 7 years).

What is the best first credit card in India for 2026?

A: For beginners, cards like the Amazon Pay ICICI Card (No Annual Fee) or the SBI SimplyClick are great starting points. If you have no income proof, ask your bank for a “Secured Card” against a Fixed Deposit.

A credit card is like a car: it can get you where you want to go faster, but you have to know how to drive it. Start small, pay in full, and watch your financial future grow.

What’s your biggest fear about credit cards? Drop a comment below, and let’s demystify it together!

Amit Sharma is the Lead Analyst at Invest With Bull, leveraging 11 years of market experience to simplify personal finance for salaried professionals. From mastering credit card arbitrage and navigating personal loans to structuring robust retirement and FIRE (Financial Independence, Retire Early) strategies, Amit provides data-backed, actionable analysis. His mission is to cut through complex banking jargon and deliver the unbiased research you need to achieve absolute financial freedom.