Axis Neo Credit Card Review 2026: Is it Really Lifetime Free?

Published: 06/02/2026 | by Amit Sharma

Axis Neo Credit Card Review 2026

Rating: ⭐⭐⭐⭐ (4/5) Best For: Students, First-time users, and “Zomato/Blinkit” addicts. Avoid If: You want travel rewards, airport lounge access, or high reward points on shopping.

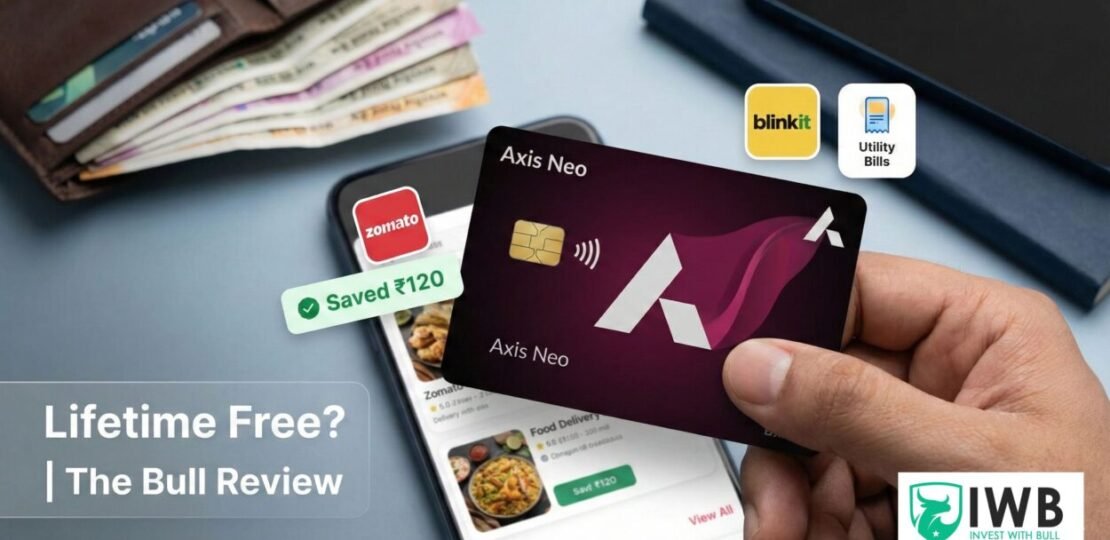

The Axis Bank Neo Credit Card is not a premium card. It is a “Utility Tool.” If you order food online or pay bills monthly, this card effectively pays you to keep it. While the reward points are poor (0.1%), the direct cash discounts on Zomato and Blinkit make it a must-have secondary card.

1. The Big Question: Is Axis Neo “Lifetime Free”?

- Official Status: No. The standard fee is ₹250 + GST per year.

- The “Lifetime Free” (LTF) Reality: Axis Bank frequently offers this card as Lifetime Free under specific conditions:

- Limited Time Offers: often visible on the official Axis Bank website banners.

- Salary Accounts: If you have an Axis salary account, you can often negotiate this as LTF.

- Select Channels: Applying through specific partner links (like Amazon or select fintech apps) can sometimes trigger the LTF offer.

Bull’s Tip: Even if you pay the ₹250 fee, you can recover this cost in just one month by using the Zomato and Blinkit offers described below.

2. Features & Benefits: The “Money Savers”

This card shines when you use it for specific apps. Here is the math on how it saves you money.

🍔 Zomato: The Hero Feature

This is the main reason to get this card.

- Offer: 40% discount (up to ₹120) per order.

- Frequency: Twice per month.

- Minimum Order: ₹200.

- Coupon Code:

AXISNEO - Potential Saving: ₹240 per month.

🛒 Blinkit (Groceries)

- Offer: 10% discount (up to ₹250).

- Frequency: Once per month.

- Minimum Order: ₹750.

- Potential Saving: ₹250 per month.

⚡ Utility Bills (via Amazon Pay/Paytm)

- Offer: 5% discount (up to ₹150) on mobile recharges, DTH, and broadband.

- Frequency: Once per month.

- Potential Saving: ₹150 per month.

🎬 Entertainment (BookMyShow)

- Offer: 10% off on movie tickets (up to ₹100).

- Note: This is a weak offer compared to other cards, but better than nothing.

3. The “Bull” Calculation: Your Real ROI

Let’s calculate the guaranteed returns if you use this card only for its partner apps.

| Spend Category | Offer Details | Monthly Saving | Annual Saving |

| Zomato | 2x Orders (₹120 off each) | ₹240 | ₹2,880 |

| Blinkit | 1x Order (10% off) | ₹250 | ₹3,000 |

| Utilities | Recharge/Broadband (5% off) | ₹150 | ₹1,800 |

| Total Savings | (Guaranteed) | ₹640 | ₹7,680 |

Analysis: Even if you pay the ₹250 annual fee, a saving of ₹7,680 gives you a massive return on investment.

4. The Drawbacks: What They Don’t Tell You

To keep this review honest (“Invest with Bull” style), you need to know the ugly side.

- Terrible Reward Rate: You earn 1 EDGE Point for every ₹200 spent.

- Translation: If you spend ₹1,00,000 on this card (non-partner apps), you earn points worth roughly ₹100. Do not use this card for regular shopping.

- Redemption Fees: When you try to redeem those tiny points, Axis charges a redemption fee (usually ₹99 + GST). This often eats up the value of the points themselves.

- No Lounge Access: This is an entry-level card. Do not expect airport perks.

- Capped Discounts: The discounts are capped (e.g., max ₹120 on Zomato). If you place a huge ₹2,000 order, the discount percentage effectively drops.

5. Comparison: Axis Neo vs. Flipkart Axis Bank

Many users get confused between these two entry-level giants.

| Feature | Axis Neo Credit Card | Flipkart Axis Bank Card |

| Annual Fee | ₹250 (Often Free) | ₹500 |

| Best For | Zomato, Blinkit, Utilities | Flipkart & Amazon Shopping |

| Reward Rate | Very Low (0.1% – 0.5%) | High (5% Cashback on Flipkart) |

| Lounge Access | No | Yes (4 Domestic/Year) |

| Verdict | Get it for Food & Bills | Get it for Shopping & Travel |

Read our full Guide: Best UPI RuPay Credit Cards 2026

6. Who Should Apply?

- The Student/Fresher: If you are new to credit, the low income eligibility makes this card easy to get.

- The “Bachelor” Lifestyle: If you live away from home and order food/groceries online frequently, this card is essential.

- The Secondary Card Holder: If you already have a premium card (like HDFC Regalia) for travel, keep this in your drawer exclusively for the Zomato/Blinkit discounts.

Read our full article about Best Credit Cards for Salaried People in India

Axis Neo Credit Card Review is not completed without Pros vs. Cons: The Honest Breakdown

| Feature | Verdict | The Bull’s Take |

| Zomato Discount | ✅ Winner | Flat 40% off (up to ₹120) twice a month. Best food offer on entry-level cards. |

| Blinkit & Bills | ✅ Winner | 10% off on Blinkit and 5% off on Utility bills (via Amazon Pay) adds real monthly value. |

| Approval Odds | ✅ High | Low income eligibility makes it perfect for students, freshers, or first-time cardholders. |

| Annual Fee | ✅ Excellent | Often available as Lifetime Free (LTF) or with a low ₹250 fee that is easily recovered. |

| Reward Rate | ❌ Fail | Only 1 point per ₹200 spent (0.1% return). This is the worst in the segment. |

| Redemption Fee | ❌ Fail | You are charged ₹99 + GST just to redeem points, eating up your already low rewards. |

| Lounge Access | ❌ Missing | No airport lounge access. Not suitable for travelers. |

| Discount Capping | ⚠️ Limit | Discounts are capped (e.g., max ₹150 on bills), so you won’t save big on huge purchases. |

Frequently Asked Questions (FAQ)

Is Axis Neo card actually free?

It is conditionally free. While the standard fee is ₹250, many users get it “Lifetime Free” during special promotional periods or if they have an Axis Bank salary account.

Does Axis Neo have lounge access?

No, the Axis Neo Credit Card does not offer complimentary airport lounge access.

What is the minimum salary for Axis Neo?

Axis Bank typically requires a net monthly income of ₹15,000 to ₹25,000 for salaried employees, making it very accessible.

Is the Zomato offer applicable on every order?

No. The Zomato discount (AXISNEO) is applicable twice per month per card.

Minimum Order Value: ₹200

Max Discount: ₹120 per order.

Pro Tip: If you have an Add-on card for a family member, they may be able to use the code separately on their Zomato account, effectively doubling your usage to 4 times a month (subject to current bank loopholes).

What are the “Hidden Charges” I should know about?

While the card is low-cost, watch out for these specific fees:

Redemption Fee: Every time you redeem your reward points, you are charged ₹99 + GST. Since the reward rate is low, only redeem when you have accumulated a large number of points.

Rent Pay Fee: 1% surcharge on all rental transactions (max ₹1,500).

Foreign Currency Markup: A standard 3.5% fee applies to international transactions. Do not use this card for international travel.

EMI Processing Fee: If you convert a purchase to EMI, a one-time processing fee of 1.5% (min ₹150) applies.

Can I increase my Axis Neo credit limit?

Yes, you can request a limit increase after 6–12 months of consistent usage.

How to check: Open the Axis Mobile App > Credit Cards > Select Card > Total Controls > Check for Limit Increase.

Manual Request: If the app shows no offer, you can email customer support with your latest salary slip or ITR to request an enhancement manually.

Can I get an Add-on card for my family?

Yes, Axis Bank allows you to apply for Add-on cards for family members (spouse, parents, siblings, or children over 18).

Fee: Usually Nil (Free) for the Neo Add-on card.

Benefit: The spend on the Add-on card counts towards your primary limit, but it helps you manage household expenses better.

Final Thoughts

The Axis Neo isn’t flashy. It won’t get you free flights. But in 2026, where inflation is hitting food and utility bills, a card that saves you flat cash on daily essentials is a winner.

Recommendation: If you can get it Lifetime Free, apply immediately. If not, check your Zomato history—if you order more than twice a month, it’s still worth the ₹250 fee.

Check your eligibility on the official Axis Bank website

Amit Sharma is the Lead Analyst at Invest With Bull, leveraging 11 years of market experience to simplify personal finance for salaried professionals. From mastering credit card arbitrage and navigating personal loans to structuring robust retirement and FIRE (Financial Independence, Retire Early) strategies, Amit provides data-backed, actionable analysis. His mission is to cut through complex banking jargon and deliver the unbiased research you need to achieve absolute financial freedom.

RELATED POSTS

View all

10 Best Zero Forex Markup Credit Cards in India (2026 Guide)

Last Updated: 23/02/2026 | by Amit Sharma